TL;DR:

- The spender versus saver dynamic shapes how individuals manage money, often resulting in internal or relationship conflicts. Practical systems like automation and real-time spending limits help balance tendencies, reducing shame and improving decision-making. Understanding personal financial behavior and using honest data can transform conflicts into opportunities for healthier money habits.

The financial spender vs saver dynamic is defined as the tension between two contrasting money orientations: one that prioritizes present enjoyment and one that prioritizes future security. This dynamic shapes every financial decision you make, from daily purchases to long-term goals. 49% of U.S. consumers maintain budgets specifically to increase savings, while 38% budget to avoid overspending. Those numbers reveal how common the internal tug-of-war between spending and saving really is. Understanding where you fall on this spectrum is the first step toward managing your money with intention rather than regret.

What is a financial spender vs saver dynamic, and why does it matter?

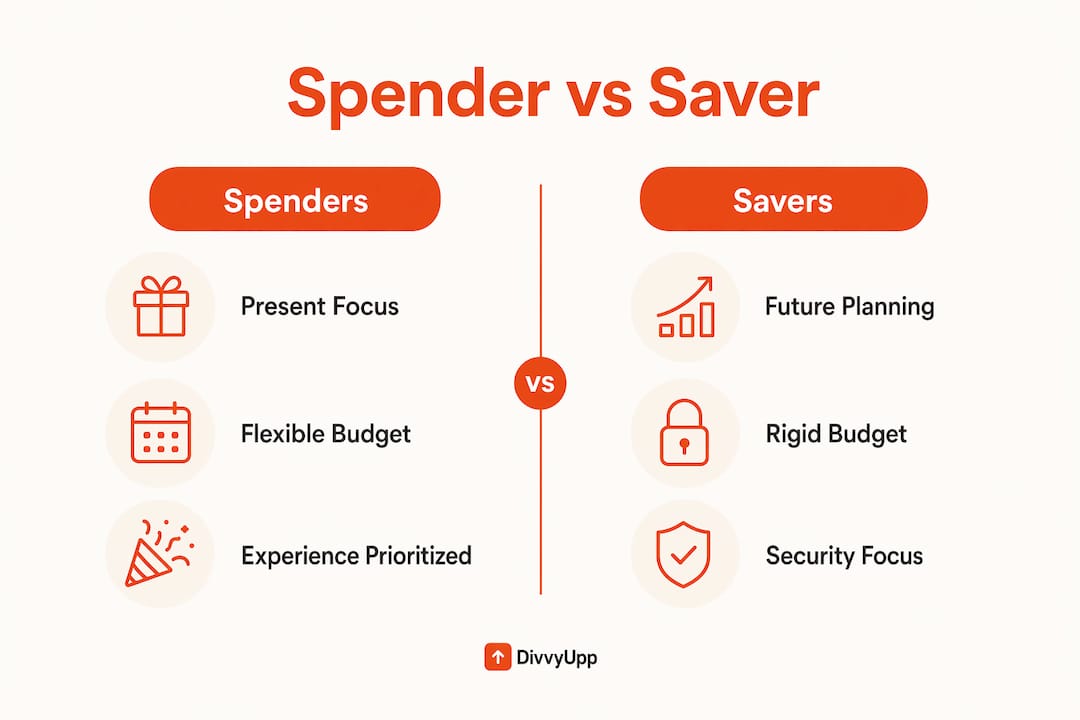

The spender vs saver dynamic describes how your core attitude toward money drives your financial decisions, often without you realizing it. Behavioral economists call these orientations “financial personality types,” and they influence everything from how you react to a sale to how much anxiety you feel checking your bank balance.

Spenders share a recognizable set of traits:

-

They prioritize present enjoyment over future security

-

They make purchases based on emotion or impulse rather than a plan

-

They value experiences, comfort, and social connection, often spending to express care for others

-

They feel restricted or anxious when forced to track every dollar

Savers operate from a different set of defaults:

-

They prioritize future stability and treat every dollar as a resource to protect

-

They budget with discipline and feel genuine discomfort spending on non-essentials

-

They derive satisfaction from watching account balances grow

-

They can tip into a scarcity mindset that limits beneficial spending

Neither orientation is wrong. The problem is when either extreme goes unchecked. A pure spender drains savings and accumulates debt. A pure saver hoards cash, misses experiences, and still feels financially anxious because the habit is driven by fear rather than confidence.

Pro Tip: Identify your default by looking at your last three months of bank statements without judgment. The pattern you see is your baseline, not your destiny.

33% of Americans report they are “just about keeping up” financially, and 22% say they are actively falling behind. Those figures suggest that most people are not operating from a position of financial confidence, regardless of which orientation they lean toward.

How do contrasting money styles create conflict and opportunity?

The spender vs saver dynamic creates the most visible friction in shared financial environments, whether that is a household, a partnership, or even your own internal conflict between this month’s fun and next year’s goals.

The emotional roots run deeper than most people expect. Tension in spender-saver dynamics often stems from mutual shame. Spenders feel judged and irresponsible. Savers feel anxious and ignored. Neither person is arguing about numbers. They are arguing about values and safety.

“The saver–spender conflict is rarely about math. It is about two people with different definitions of what money is for. One sees it as a tool for living now. The other sees it as protection against an uncertain future. Both are right. Neither can see it.”

This is why rigid budgeting systems often fail in shared contexts. When one person controls all spending decisions, the other feels policed. Hybrid financial systems that separate shared expenses from personal spending reduce daily friction and preserve individual autonomy. The practical version looks like this:

-

A joint account covers rent, utilities, groceries, and shared goals

-

Each person keeps a personal account for discretionary spending, no questions asked

-

Both parties agree on savings targets before dividing what remains

The opportunity in contrasting money styles is real. Spenders push savers to enjoy the present and invest in experiences that build relationships and well-being. Savers push spenders to think ahead and avoid the stress of financial instability. When both orientations communicate honestly, they produce better financial decisions than either would alone.

29% of U.S. consumers save specifically for named goals like a vacation or a home deposit. That specificity matters. Shared goals give spenders a reason to save and give savers permission to spend.

What practical strategies balance spender and saver tendencies?

Balancing spending vs saving habits does not require becoming a different person. It requires building systems that work with your natural tendencies rather than against them.

1. Automate savings before you see the money

Financial experts recommend moving 3–5% of income automatically to savings before it hits your spending account. For spenders, this removes the decision entirely. Money that never appears in your checking balance cannot be spent impulsively. For savers, automation confirms the goal is covered, which reduces the anxiety that drives over-restriction.

2. Create a “fun money” category

Savers often feel guilty spending on anything non-essential, even when they can afford it. A dedicated discretionary budget, a fixed amount each month with no tracking required, gives savers explicit permission to spend. This “fun money” approach reduces the psychological cost of enjoyment and prevents the resentment that builds when saving feels like permanent deprivation.

3. Align spending with your stated values

A well-calibrated sense of future regret is one of the most effective money management tools available. Before any significant purchase, ask: “Will I regret spending this, or will I regret not spending it?” Framing saving as buying financial independence rather than denying yourself pleasure shifts the emotional equation for spenders. Framing intentional spending as an investment in well-being does the same for savers.

4. Use a daily safe-to-spend number

Most budgeting approaches ask you to categorize spending after the fact. That is too late. DivvyUpp gives you a single daily number showing what is actually safe to spend today, this week, and this month, based on your real spending rate against the days left in your cycle. When you ask “can I afford this?” you get a direct answer: safe, risky, or yes-but-here’s-the-cost. Your money stays in your own bank. DivvyUpp never moves funds. That kind of real-time clarity is what spenders need to pause before overspending, and what savers need to feel confident spending without guilt.

| Strategy | Best for | Core benefit |

|---|---|---|

| Automated savings transfer | Spenders | Removes the decision; builds discipline passively |

| Fun money budget | Savers | Reduces guilt; prevents spending anxiety |

| Value-aligned spending check | Both | Connects purchases to personal priorities |

| Daily safe-to-spend number | Both | Real-time clarity before the decision, not after |

Pro Tip: Set your automated savings transfer for the same day as your paycheck deposit. You will never miss money you never see in your spending account.

What financial personality types exist beyond spender and saver?

The binary of spender vs saver is a useful starting point, but most people are more complex. Financial personality types include at least four recognizable profiles, and most people blend more than one.

-

The spender spends freely, often emotionally, and struggles to build savings without external structure

-

The saver accumulates money carefully, sometimes to the point of avoiding necessary or enjoyable spending

-

The spreadsheeter tracks every dollar obsessively, finds comfort in data, and can become paralyzed by analysis rather than action

-

The shopper spends for the experience of buying rather than the item itself, often cycling through purchases and returns

These profiles overlap and shift over time. A spreadsheeter who loses a job may become a saver. A saver who reaches financial independence may become a more intentional spender. Personality labels are starting points, not fixed states. The goal is to borrow strengths from each type rather than stay locked in one pattern.

The most financially healthy people combine the saver’s discipline with the spender’s willingness to invest in experiences, the spreadsheeter’s awareness with the shopper’s ability to enjoy the act of choosing. Many savers carry a scarcity mindset that limits beneficial spending, even when their balance sheet is strong. Intentional spending aligned with personal values, buying back time, investing in health, funding meaningful experiences, produces measurable gains in well-being that pure saving cannot.

Key Takeaways

The financial spender vs saver dynamic is not a fixed personality conflict. It is a spectrum of behaviors that can be understood, adjusted, and balanced through honest self-awareness and practical systems.

| Point | Details |

|---|---|

| Dynamic is a spectrum | Most people blend spender and saver traits rather than fitting one extreme. |

| Mutual shame drives conflict | Spenders feel judged; savers feel anxious. Naming this breaks the cycle. |

| Automation beats willpower | Moving savings automatically before spending removes the hardest decision. |

| Fun money reduces guilt | A fixed discretionary budget gives savers permission to spend without anxiety. |

| Real-time clarity changes behavior | Knowing your safe-to-spend number before a purchase prevents overspending at the source. |

Why I think the spender vs saver framing misses the real problem

I built DivvyUpp because I was the spender in my own story. Good income, real goals, and still losing the month to small decisions that felt fine in the moment and terrible on the statement. I tried every budgeting method. The problem was never the plan. The problem was the gap between making a decision and knowing its cost.

Most financial advice treats spenders and savers as fixed types who need to meet in the middle. I disagree. The real issue is that almost nobody, spender or saver, has accurate real-time information when they are actually deciding whether to spend. Savers restrict themselves based on anxiety, not data. Spenders overspend because they genuinely do not know where they stand until it is too late.

What changed my behavior was not a budget category or a savings rule. It was a single number: what is actually safe to spend today? That question, answered honestly and updated daily, removed the guesswork from both sides. Spenders get permission when they have room. Savers get confirmation that spending will not wreck the month. The dynamic does not disappear, but it stops being a source of shame and starts being something you can actually manage.

The uncomfortable truth is that most financial conflict, internal or interpersonal, is not about values. It is about information. When two people each know their own safe-to-spend number, the conversation shifts from “you spent too much” to “here’s what I have left.” That is a solvable problem.

— Srini / Founder @ DivvyUpp

What DivvyUpp does for your daily spending decisions

Understanding your financial personality type is useful. Acting on it in real time is what actually changes your bank balance.

DivvyUpp is built for people who have real financial goals but keep losing ground to flexible, unplanned spending. It gives you a single daily safe-to-spend number based on your actual spending rate against the days left in your cycle. No categories to build. No transactions to log after the fact. Just a direct answer when you need it: safe, risky, or yes-but-here’s-the-cost. Your money stays in your own bank — DivvyUpp is non-custodial and read-only, so it never moves your funds. Try it free with a no-signup demo.

General information, not financial advice.

FAQ

What is the financial spender vs saver dynamic?

The financial spender vs saver dynamic describes the contrast between two money orientations: spending for present enjoyment versus saving for future security. It influences financial decisions, budgeting habits, and interpersonal money conflicts.

Can a person be both a spender and a saver?

Yes. Financial personality types exist on a spectrum, and most people blend traits from multiple profiles. Labels are starting points, not fixed identities.

Why do spenders and savers clash so often?

Conflict between spenders and savers typically stems from mutual shame rather than numerical disagreement. Spenders feel judged; savers feel anxious. Honest communication about values, not just budgets, resolves most of the friction.

What is the “pay yourself first” strategy?

“Pay yourself first” means automatically transferring a set percentage of income to savings before it reaches your spending account. Financial experts recommend starting at 3–5% of income to build discipline without requiring constant willpower.

How does knowing your safe-to-spend number help balance spending and saving?

A daily safe-to-spend number tells you exactly how much room you have before a purchase, removing the guesswork that causes both overspending in spenders and unnecessary restriction in savers. DivvyUpp calculates this number in real time so your decision is based on data, not anxiety.