A daily spending limit for savings goals is the maximum discretionary amount you allocate each day after covering fixed expenses and planned savings. This number is not your bank balance. It is a calculated ceiling that tells you exactly how much you can spend without derailing your financial targets. Financial experts recommend saving 15–20% of gross income toward savings and debt repayment. The 50/30/20 rule formalizes this by splitting income into 50% needs, 30% wants, and 20% savings. Your daily spending limit lives inside that 30% “wants” bucket, broken into a number you can actually use each morning.

What is a daily spending limit for savings goals?

A daily spending limit is a discretionary ceiling, not a suggestion. The most common mistake people make is treating their checking account balance as permission to spend. Your balance includes rent, utilities, subscriptions, and your savings target. None of that money is yours to spend freely.

The 50/30/20 budgeting rule gives you the clearest framework. After allocating 50% to needs and 20% to savings or debt, the remaining 30% becomes your discretionary pool. Divide that monthly pool by the number of days in the month, and you have your daily allowance. That single number converts an abstract monthly budget into a concrete daily decision.

Daily tracking turns vague financial goals into specific daily numbers, which improves both decision-making and motivation. When you know your limit is $42 today, you make different choices at lunch than when you think “I still have $1,200 left this month.”

How do you calculate your daily spending limit?

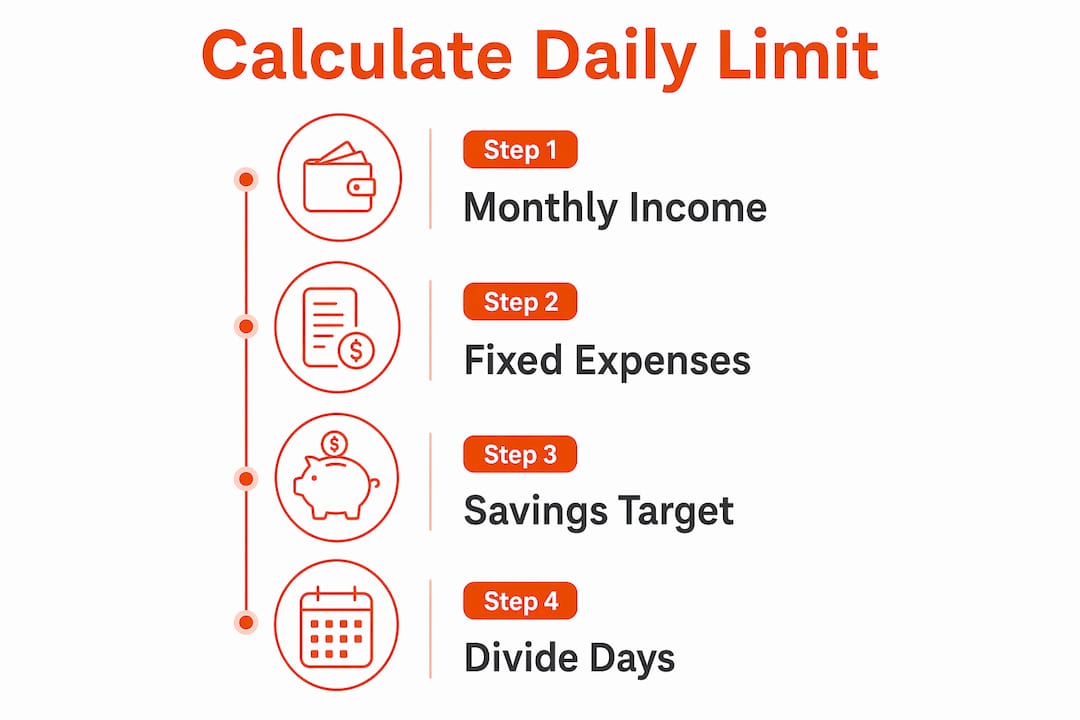

The calculation follows four steps. Get each one right, and the number you land on will actually work.

Step 1: Find your monthly net income. Use take-home pay, not gross. This is the money that actually hits your account.

Step 2: Subtract fixed monthly expenses. Include rent or mortgage, utilities, insurance, loan minimums, and every subscription. Be thorough. Most people undercount subscriptions by $50–$100 per month.

Step 3: Subtract your savings target. Apply the 15–20% gross income benchmark here. If your gross is $5,000 and you target 20%, that is $1,000 per month going directly to savings or debt.

Step 4: Divide by days in the month. The result is your daily spending allowance for discretionary purchases only.

The table below shows how this plays out across three common income and goal scenarios.

| Scenario | Monthly net income | Fixed expenses | Savings target | Discretionary pool | Daily limit |

|---|---|---|---|---|---|

| Single, debt payoff focus | $3,200 | $1,800 | $640 | $760 | $25 |

| Couple, FIRE goal | $6,500 | $3,000 | $1,300 | $2,200 | $73 |

| Single, emergency fund | $4,000 | $2,100 | $600 | $1,300 | $43 |

These numbers are starting points, not permanent rules. Your actual fixed costs and savings rate will shift the daily limit up or down.

Pro Tip: Track every expense for 30 days before locking in your limit. Most people discover $150–$300 in monthly spending they did not consciously choose, which frees up real room in the daily allowance.

How do you implement and stick to your daily limit?

Knowing your number means nothing if you do not build a system around it. Three methods work consistently well.

Automate savings on payday

The “pay yourself first” method transfers your savings target automatically the moment your paycheck arrives. This removes the decision entirely. You never see the money as available to spend, so willpower is not a factor. Automating savings is the single most reliable way to maintain consistent progress toward any financial goal.

Use real-time spending alerts

Financial stress comes more from small impulsive purchases and subscription fatigue than from large planned expenses. Monthly reviews catch these patterns too late. A daily budget planner or spending alert system shows you where you stand before you make the next purchase, not after the statement arrives. Divvyupp takes this further by giving you a single “safe to spend” number each day based on your actual spending rate against the days left in your cycle.

Audit your subscriptions

It’s surprisingly easy to lose a chunk of your income to subscriptions you’ve forgotten you’re paying for. Canceling services you do not actively use raises your daily limit immediately without changing your lifestyle. Run a subscription audit every quarter. Cancel anything you have not used in the past 30 days.

-

Apply the 24-hour rule before any non-essential purchase over $30. Sleep on it. Most impulse buys lose their appeal by morning.

-

Keep a separate account for discretionary spending. When that account is empty, spending stops. The visual boundary works better than mental math.

-

Set a weekly check-in, not just a monthly review. Weekly checks catch problems while they are still small.

Pro Tip: Separate your spending account from your savings account at the bank level. When the discretionary account hits zero, you stop. No mental math required.

What challenges will you face, and how do you fix them?

Sticking to a daily limit is a behavioral challenge as much as a math problem. The obstacles are predictable, which means the fixes are too.

A 30-day review period reveals patterns in irregular expenses like quarterly subscriptions, emotional spending spikes, and payday timing gaps. Without this review, your daily limit will feel wrong because it is based on incomplete data. Run the full month before judging whether your limit is realistic.

The table below maps the most common challenges to their root causes and practical fixes.

| Challenge | Root cause | Fix |

|---|---|---|

| Impulsive purchases | Emotional triggers, boredom | 24-hour rule, spending checklist |

| Subscription fatigue | Forgotten recurring charges | Quarterly audit, bank alert for new charges |

| Irregular expenses | Quarterly or annual bills | Divide annual costs by 12, add to fixed expenses |

| Limit feels too tight | Savings target set too high | Reduce savings rate temporarily, rebuild gradually |

| Partner disagreement | Different spending values | Shared daily limit with individual “no questions asked” allowances |

The motivational case for pushing through these challenges is concrete. Cutting $60 in weekly discretionary spending saves more than $3,000 per year. That is a meaningful emergency fund, a debt payoff, or a year of retirement contributions from one behavioral shift.

Build an emergency buffer of $200–$500 in your spending account. This covers genuine surprises without forcing you to raid your savings. The buffer prevents the all-or-nothing thinking that causes people to abandon their budget after one bad week.

How do you tailor daily limits for multiple goals and life stages?

Most people carry more than one financial goal at the same time. A single daily limit needs to serve all of them without creating confusion.

The clearest approach is to prioritize by urgency and timeline. Debt with high interest costs you money every day you carry it, so it ranks above discretionary savings goals. An emergency fund protects every other goal, so it comes second. Retirement savings and special purchases follow after those foundations are in place.

-

Debt payoff phase: Direct 20–25% of net income to debt minimum payments plus extra principal. Keep the daily discretionary limit tight until high-interest balances clear.

-

Emergency fund phase: Once debt is under control, redirect the extra payment toward a three-to-six-month expense buffer. Your daily limit stays the same. The destination of the savings changes.

-

FIRE or early retirement goal: Couples pursuing financial independence often target savings rates of 40–60% of net income. This compresses the daily discretionary limit significantly. Both partners need to agree on the number and understand the tradeoff.

-

Couples with shared finances: Assign a shared daily limit for household discretionary spending and a separate individual allowance for each partner. This prevents resentment and keeps both people accountable without micromanaging each other’s choices.

-

Life stage shifts: A job change, new child, or paid-off loan changes your fixed expenses and income. Recalculate your daily limit any time one of these events occurs. Do not wait for the annual review.

The daily limit is not a fixed rule. It is a number that reflects your current income, current goals, and current life. Adjust it when your situation changes, and treat the adjustment as progress, not failure.

Key Takeaways

Setting a daily spending limit for savings goals works because it converts abstract monthly budgets into a single number you can act on every day.

| Point | Details |

|---|---|

| Calculate your daily limit correctly | Subtract fixed expenses and your savings target from net income, then divide by days in the month. |

| Automate savings first | Transfer savings on payday so the money is never available to spend impulsively. |

| Use real-time tracking | Daily spending alerts catch overspending before it happens, not after the statement arrives. |

| Audit subscriptions quarterly | Unused subscriptions consume budget silently; canceling them raises your daily limit immediately. |

| Adjust limits as life changes | Recalculate your daily allowance after any income shift, new goal, or major expense change. |

Why daily limits beat monthly budgets every time

I have watched people build detailed monthly budgets in spreadsheets and abandon them by the 10th of the month. The problem is not discipline. The problem is that a monthly number is too abstract to guide a Tuesday afternoon purchase decision.

A daily limit solves this. When you know you have $43 to spend today, you make a real choice at the coffee shop, the grocery store, and the online checkout. The monthly budget sits in a spreadsheet. The daily limit sits in your head, or better yet, on your phone screen before you tap “buy.”

The behavioral shift I find most underrated is the subscription audit. People treat subscriptions as fixed expenses, but most are not truly fixed. They are just forgotten. Freeing $80 per month from unused services is the equivalent of a $1 raise in your daily limit. That is not a small thing when your limit is $30.

For couples, the daily limit conversation is actually a values conversation. When you sit down and agree on a number, you are agreeing on what matters. That agreement is worth more than any spreadsheet formula.

The hardest part is the first 30 days. Your initial limit will feel wrong because your data is incomplete. Stick with it. Track everything. Adjust after the first full month. By day 60, the limit stops feeling like a restriction and starts feeling like information.

— Srini / Founder @ DivvyUpp

How Divvyupp makes your daily limit work automatically

Setting a daily spending limit on paper is straightforward. Knowing whether you have hit it by 2:00 PM on a Wednesday is harder. That is the gap Divvyupp fills.

Divvyupp calculates your safe-to-spend number each day based on your actual spending rate against the days remaining in your billing cycle. You do not build a budget plan or categorize transactions after the fact. You get one number: safe, risky, or yes-but-here-is-the-cost. Your money stays in your own bank. Divvyupp does not move funds. It just answers the question you are already asking before every purchase. Free to try, no signup required.

FAQ

What is a daily spending limit for savings goals?

A daily spending limit for savings goals is the maximum discretionary amount you can spend each day after covering fixed expenses and transferring your planned savings. It converts your monthly budget into a number you can use for every purchase decision.

How do I calculate my daily spending allowance?

Subtract your fixed monthly expenses and savings target from your monthly net income, then divide the remaining amount by the number of days in the month. The result is your daily discretionary ceiling.

How much of my income should I save each day?

Financial experts recommend saving 15–20% of gross income. Under the 50/30/20 rule, 20% goes to savings and debt repayment before you calculate your daily spending allowance from the remaining funds.

Does a daily limit work for couples with different spending habits?

A shared daily limit for household expenses combined with individual “no questions asked” allowances for each partner gives both people autonomy while keeping the household on track. Recalculate the shared limit any time income or fixed expenses change.

How often should I review and adjust my daily spending limit?

Run a weekly check to catch impulsive spending patterns early, and do a full monthly review to capture irregular expenses like quarterly bills and subscription charges. Recalculate your limit immediately after any major income or expense change.

This is general information, not financial advice — just what’s worked for me.

Recommended